The Case for Medigap Plan N: 5 Reasons It Appeals to Today’s Healthier Retirees

As a Medicare broker, I help clients weigh their options carefully - not just when they first enroll, but as their health, budget, and Medicare landscape evolve. Over the last few years, one of the biggest shifts we’ve seen in Medicare supplement (Medigap) choices is the growing appeal of Medigap Plan N - especially for retirees who are generally healthy and want to balance solid coverage with manageable premiums.

While Plan G has long been considered the “gold standard” after Plans F and C were phased out for new enrollees, Plan N is increasingly emerging as a practical and stable alternative for many beneficiaries. Let’s take a closer look at why that is, especially in a population that’s healthier and more engaged with preventive care than ever before.

Medigap Basics: What Plans G and N Cover

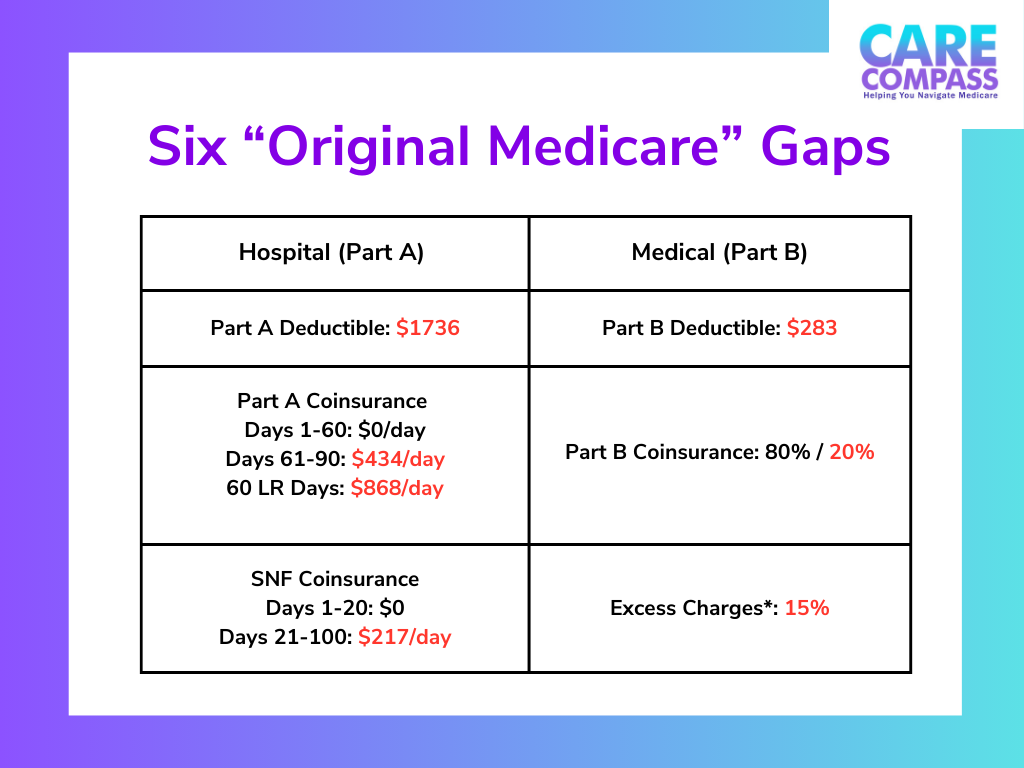

Both Plan G and Plan N are Medigap (Medicare Supplement) policies that work with Original Medicare (Parts A & B) to help pay for out-of-pocket costs - AKA “Gaps” that are left by Original Medicare - like deductibles, coinsurance, and copayments. Below is a visual of the major “gaps” in Original Medicare coverage. The numbers listed in red would be the responsibility of the Medicare enrollee should s/he not have a Medigap plan to cover those costs.

Six Medicare Gaps in 2026. These numbers are subject to change yearly. *Excess charges are not allowed in some states (like Pennsylvania).

Because Medicare doesn’t have a cap on out-of-pocket spending, Medigap plans bring predictability and peace of mind to many seniors.

Neither a Plan G nor a Plan N covers the Part B deductible ($283 in 2026), however they both cover:

Part A deductible

Part A hospital coinsurance

Skilled nursing facility coinsurance

Part B coinsurance

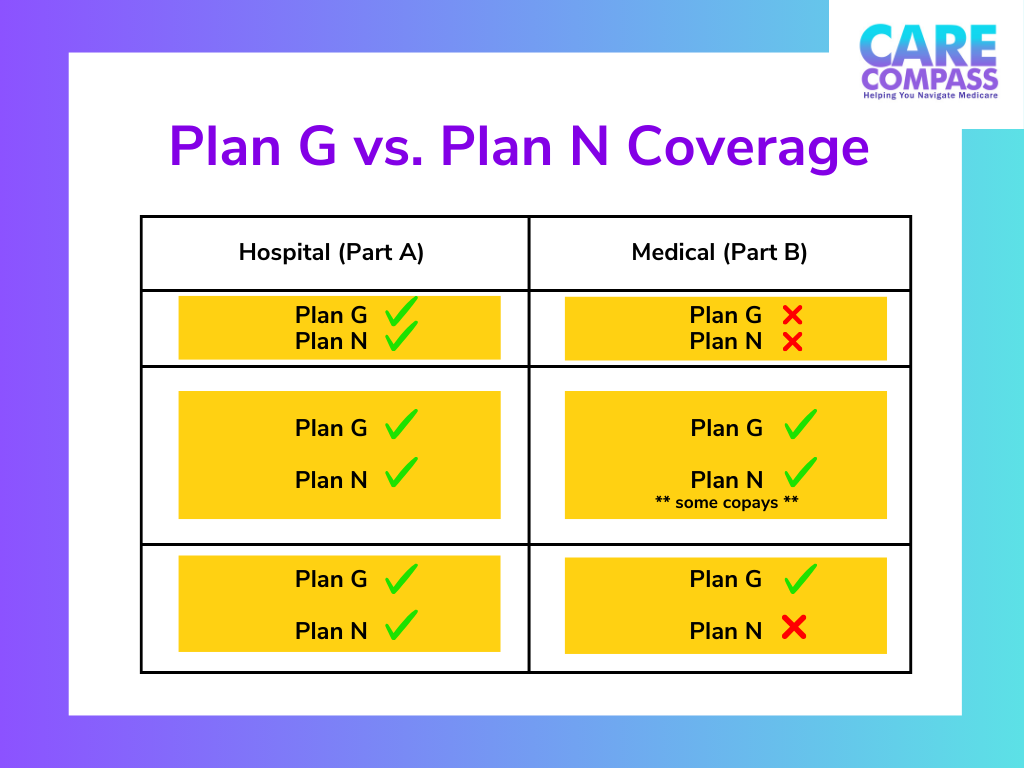

Key Differences

Plan G covers Medicare Part B excess charges.

Plan N does NOT cover excess charges and may require small copays for doctor visits ($20) and ER ($50) visits that do not result in a hospital admission.

Medigap Plan G vs. Plan N Coverage.

Why Plan N Could Be A Safer Option for a Healthy Population

1. Lower Premiums Without Sacrificing Core Coverage

One of the biggest reasons beneficiaries choose Plan N is the premium savings.

Plan N generally carries lower monthly premiums than Plan G - often significantly so - because it shifts a small amount of cost sharing back to the enrollee via predictable copays (e.g., up to $20 for most doctor visits and up to $50 for ER visits not resulting in hospital admission).

For a healthy retiree who visits the doctor occasionally, the premium savings often outweigh the nominal copays they might pay throughout the year, especially when they infrequently use medical services.

2. Most Providers Accept Medicare Assignment

The biggest coverage difference - Part B excess charges - is only relevant if a provider does NOT accept Medicare assignment (meaning they can bill up to 15% above the Medicare-approved rate).

But here’s the key point: the vast majority of Medicare providers "accept assignment”, meaning excess charges are rare in most areas. In some states (like Pennsylvania), excess charges are prohibited entirely, which effectively eliminates this concern for Plan N enrollees.

For healthier retirees who choose providers within the Medicare assignment network, this makes Plan N’s coverage essentially on par with Plan G in practical terms.

3. Healthier Risk Pool

Another reason Plan N can be appealing long-term is who typically enrolls in the plan.

In certain circumstances, called Guaranteed Issue periods (not to be confused with Medigap Open Enrollment Period), Medicare beneficiaries can enroll in a Medigap plan without medical underwriting (medical questions). This usually happens when current coverage ends - for example, if a Medicare Advantage plan terminates, a beneficiary moves out of the plan’s service area, or a Medigap insurance company goes out of business.

In most Guaranteed Issue situations, beneficiaries have guaranteed access to Medigap Plan G, while Plan N is typically excluded. This means that many people who have ongoing medical conditions are entering into Plan G with no medical questions asked, increasing usage, carrier costs, and ultimately, premiums.

By contrast, many individuals who enroll in Plan N outside of their Medigap Open Enrollment Period do so voluntarily and are subject to medical underwriting, which typically means they are healthier at the time of enrollment.

Over time, this enrollment pattern can result in a healthier overall risk pool for Plan N, while Plan G more often serves as the default option for individuals who need guaranteed acceptance due to higher medical usage. This difference may help support Plan N’s stability over the long run.

4. Healthier Retirees Tend to Use Less Care

With better overall health and preventive care, many retirees visit doctors less often than in the past.

This trend, partly driven by lifestyle improvements and earlier detection of chronic conditions, means:

Lower annual utilization of healthcare services

Fewer ER visits and specialist appointments

Fewer surprises in copays or unexpected bills

For this group, predictable, modest copays can be an acceptable trade-off for reduced monthly premiums.

Let’s illustrate:

If Plan N’s premium is $25–$40 cheaper per month, that’s $300–$480 in annual savings. If you only go to the doctor 6–8 times per year at a $20 copay per visit, your total copays are $120-$160 a year, far less than the premium savings.

5. Budget Predictability with Copays vs. Risk of Rising Premiums

Premiums are almost always the number one concern for Medicare beneficiaries on a fixed income. Many clients tell me that reducing guaranteed monthly outlay improves financial confidence even if it comes with small, predictable costs.

That stability can feel “safer” than paying a higher premium year after year, especially when historical data shows Plan G premiums often escalate faster over time than Plan N.

Who Might Still Prefer Plan G?

To be fair, Plan G may be the better choice for some beneficiaries, particularly those who:

See multiple specialists often

Do not want to deal with any copayments

May be exposed to excess charges

Prefer strict cost containment above all else

Plan G eliminates copays and protects against excess charges, making it a very predictable plan for high-utilizers. But for a low-to-moderate utilization retiree with good health and providers who accept assignment, Plan N represents a smart, budget-focused alternative.

Summary

For many healthy retirees, Medigap Plan N strikes a strong balance between coverage and cost. It provides most of the same protections as Plan G, but with lower monthly premiums and predictable copays that are often manageable for those who don’t visit the doctor frequently.

Because excess charges are uncommon in many areas and Plan N is typically chosen by healthier applicants, the plan can offer both short-term savings and long-term stability. While Plan G may still make sense for beneficiaries with higher medical needs, Plan N has become a smart, budget-conscious choice for retirees who want solid coverage without paying for benefits they may not use.

If you need help navigating your Medicare supplement options in Blair County, PA or the surrounding region, contact Care Compass today to schedule your NO COST consultation!

Care Compass is an independent insurance agency that helps seniors navigate the complexities of Medicare and other Senior Products. Our services are offered at NO COST! Care Compass is proudly owned and operated in Blair County, Pennsylvania. We provide Medicare insurance assistance to the residents of Altoona, Hollidaysburg, Duncansville and the surrounding region. If you need assistance with Medicare, contact Care Compass today!