IRMAA Explained: Why Some Medicare Beneficiaries Pay More (and What You Can Do About It)

If you are approaching 65 or already enrolled in Medicare, you probably know that Medicare isn't entirely free. Most people pay a standard monthly premium for Medicare Part B (which covers doctors and outpatient services) and a separate premium for their Part D prescription drug plan.

But what happens if you open your mail and discover that the Social Security Administration is charging you significantly more than the standard rate ($202.90 in 2026)?

If this happens to you, you have likely been hit with IRMAA - the Income-Related Monthly Adjustment Amount. At Care Compass, we sit down with retirees across Blair County and Central PA who are completely caught off guard by this surcharge. Often, it's triggered by a one-time financial event, like selling a property or taking a large retirement distribution.

Here is everything you need to know about what IRMAA is, how it is calculated, and most importantly, how you might be able to appeal it.

📌 If you are just starting your Medicare journey, we highly recommend reading our comprehensive blog, A Beginner's Guide to Medicare: What It Is, How It Works, and Where to Start, to get a full overview of how the program works.

What is IRMAA?

IRMAA stands for the Income-Related Monthly Adjustment Amount. It is an extra surcharge added to your Medicare Part B and Part D premiums if your income is above a certain threshold.

In 2026, the standard Medicare Part B premium is $202.90 per month. However, if your income places you in an IRMAA bracket, you will pay that standard premium plus an additional surcharge. This surcharge also applies to your Part D prescription drug coverage, meaning you will pay an extra amount on top of your regular plan premium.

These surcharges are automatically deducted from your monthly Social Security check. If you are not yet receiving Social Security benefits, you will receive a separate bill directly from Medicare.

How is IRMAA Calculated?

The most confusing part about IRMAA is the timeline. The Social Security Administration (SSA) determines your IRMAA status by looking at your tax return from two years prior. For example, to determine your 2026 Medicare premiums, the SSA will look at the tax return you filed in 2025 for the 2024 tax year.

They calculate this using your Modified Adjusted Gross Income (MAGI), which is your Adjusted Gross Income plus any tax-exempt interest income. If your MAGI from two years ago crosses the threshold, you get hit with the surcharge.

Here is where many people get blindsided: you do not have to be a high earner to trigger IRMAA. We frequently see Blair County residents get hit with this surcharge because of a single one-time financial event like selling a family home, cashing in a large CD, or taking a lump-sum distribution from an IRA. Because the SSA looks two years back, that one-time spike in income can affect your Medicare premiums long after the money is gone. If you are planning a major financial transaction in retirement, it is worth understanding the potential Medicare impact before you act.

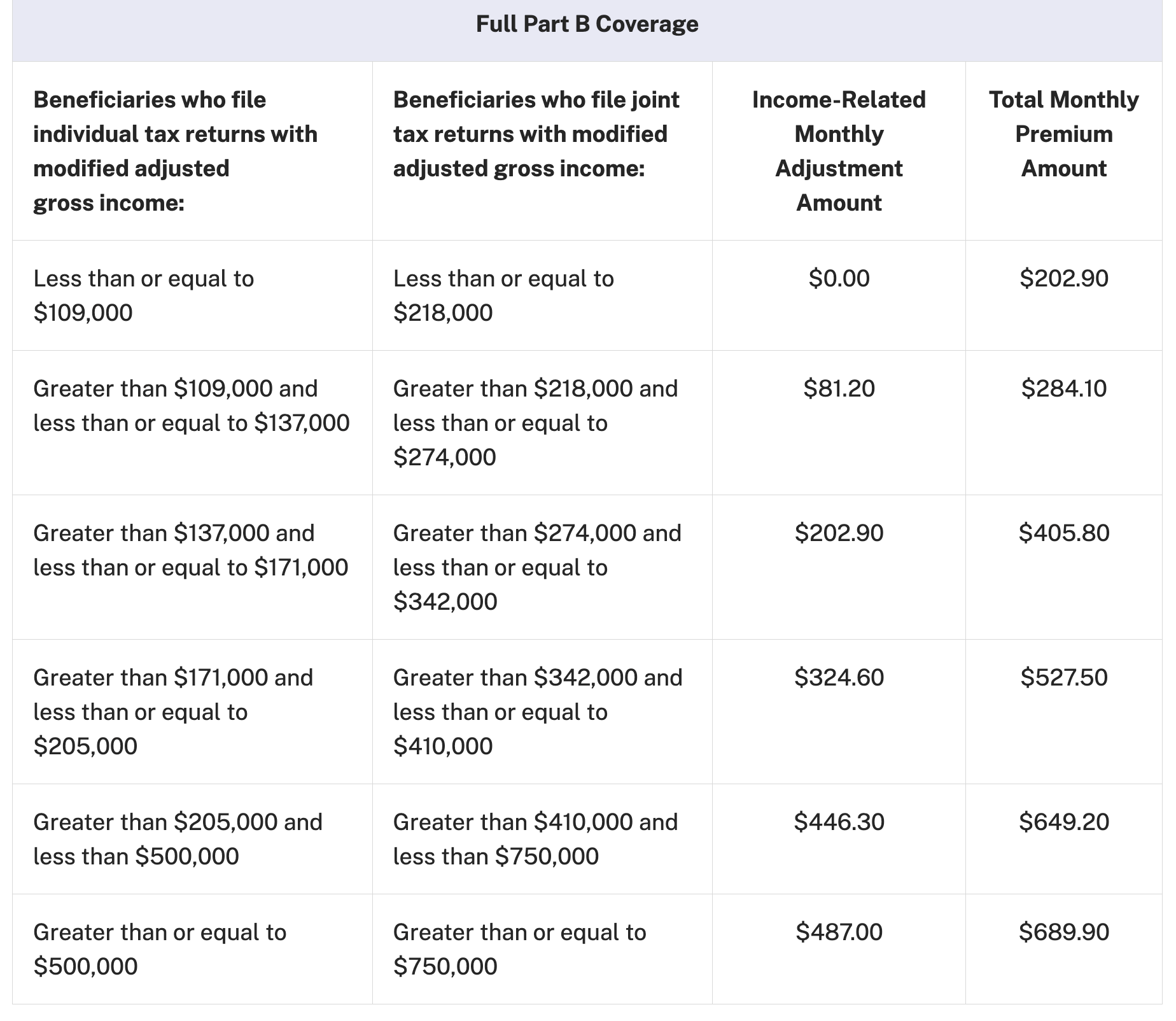

The 2026 IRMAA Income Brackets

For 2026, the IRMAA surcharge kicks in if your individual income is above $109,000, or if your joint income (married filing jointly) is above $218,000. Here is a breakdown of the 2026 Part B brackets:

2026 IRMAA Chart - Source: CMS.gov

Note: These brackets also trigger an additional surcharge for your Part D prescription drug plan, ranging from an extra $14.50 to $94.10 per month depending on your tier. You can learn more here.

Can You Appeal IRMAA?

Yes! This is the most important thing to know about IRMAA. Because the SSA looks at your income from two years ago, that number may not accurately reflect your financial reality today.

If your income has significantly decreased due to a Life-Changing Event, you can file an appeal to have your IRMAA surcharge reduced or eliminated. The Social Security Administration recognizes eight specific Life-Changing Events:

Marriage

Divorce or annulment

Death of a spouse

Work stoppage (e.g., you retired)

Work reduction (e.g., you transitioned to part-time)

Loss of income-producing property due to a disaster or event beyond your control

Loss or reduction of pension income

An employer settlement payment due to closure or bankruptcy

If you experienced one of these events and your income has dropped, you can file Form SSA-44 (Medicare Income-Related Monthly Adjustment Amount – Life-Changing Event). You will need to provide documentation of the event (like a letter from your employer stating your retirement date) and an estimate of your current, lower income.

Summary

Getting an IRMAA notice in the mail can be frustrating, but it doesn't have to be permanent. IRMAA is recalculated every single year. If your income drops back below the threshold, your premium will automatically return to the standard rate the following year. And if you've experienced a qualifying life-changing event, you don't have to wait - you can appeal right away. If you are also wondering whether a life event affects your ability to change your Medicare plan, read Medicare Special Enrollment Periods Explained.

Navigating Medicare costs can be complicated, but you don't have to do it alone. If you live in Altoona, Hollidaysburg, Duncansville, or the surrounding region and need help understanding your Medicare options, schedule a NO COST consultation with Care Compass today!

Care Compass is an independent insurance agency that helps seniors navigate the complexities of Medicare and other Senior Products. Our services are offered at NO COST! Care Compass is proudly owned and operated in Blair County, Pennsylvania. We provide Medicare insurance assistance to the residents of Altoona, Hollidaysburg, Duncansville and the surrounding region. If you need assistance with Medicare, contact Care Compass today!