Which is Better: Medicare Advantage or a Medicare Supplement?

If you are approaching 65 and starting to research your Medicare options, you have likely realized that Original Medicare (Parts A and B) doesn't cover everything. To protect yourself from unexpected medical bills, you have to make a choice between two very different paths: Medicare Advantage or a Medicare Supplement (Medigap). This is the single biggest decision you will make regarding your healthcare in retirement.

At Care Compass, we sit down with residents across Blair County and Central PA every day to help them make this exact choice. While both options have their place, they operate very differently. Here is our honest, head-to-head comparison to help you decide which path is right for you.

Before we compare the two paths, if you're brand new to Medicare, we recommend reviewing A Beginner's Guide to Medicare: What It Is, How It Works, and Where to Start).

The Core Difference: "Pay Now" vs. "Pay As You Go"

The easiest way to understand the difference between a Supplement and an Advantage plan is how you pay for your healthcare.

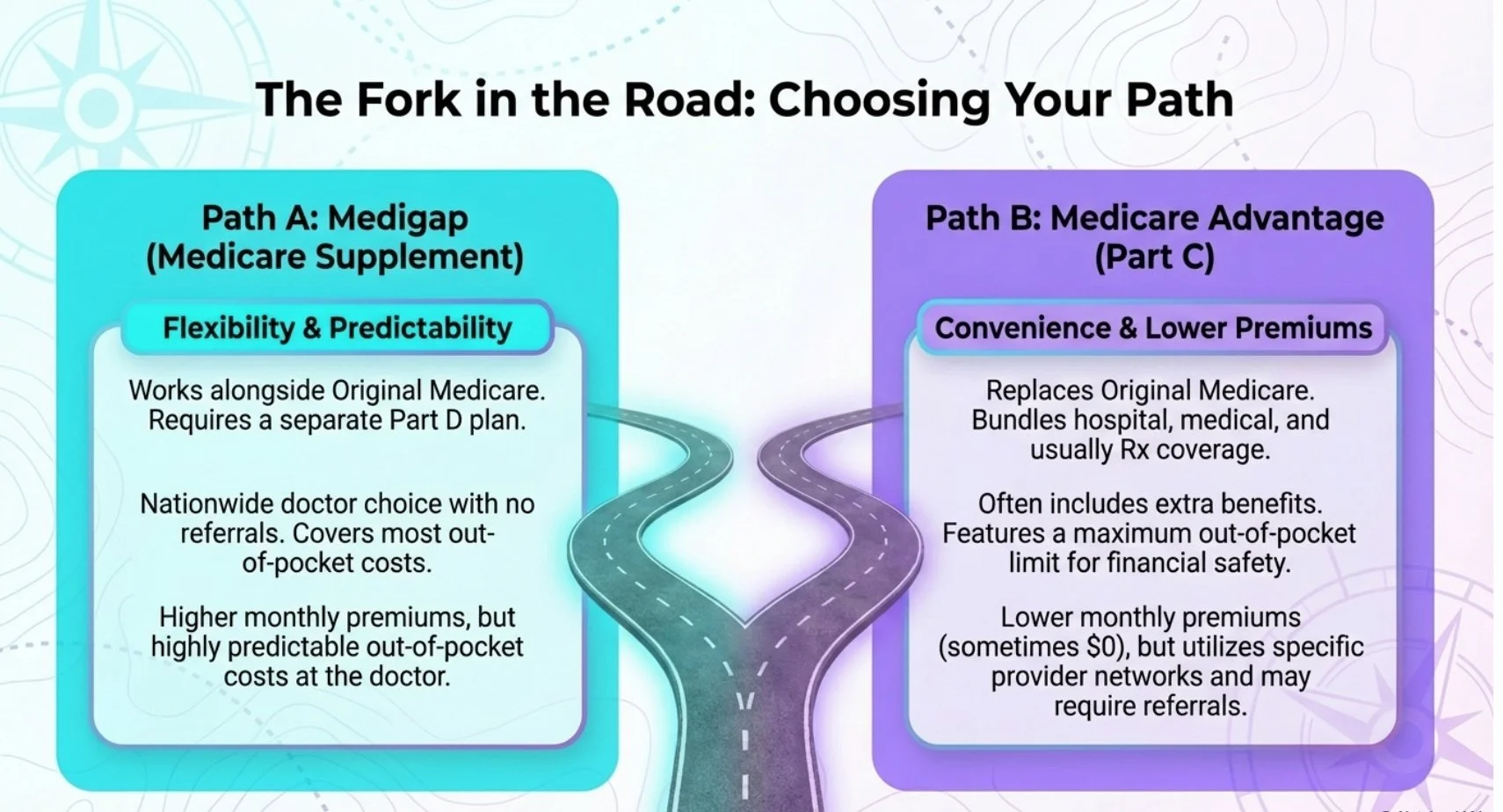

Medicare Supplements (Medigap) are a "Pay Now" system. You pay a higher monthly premium upfront. In exchange, the insurance company pays almost all of your approved medical bills. You have very little out-of-pocket exposure when you actually go to the doctor or hospital.

Medicare Advantage (Part C) is a "Pay As You Go" system. You pay a very low (sometimes $0) monthly premium upfront. However, when you use healthcare services - like visiting a specialist, getting an MRI, or staying in the hospital - you pay copays and coinsurance out of your own pocket.

The Case for Medicare Supplements (Medigap)

At Care Compass, we often emphasize that Medigap plans provide the most comprehensive coverage with the lowest financial risk.

When you purchase a Medigap plan (like Plan G or Plan N), it acts as a secondary payer to Original Medicare. Medicare pays its share of the bill (usually 80%), and your Supplement steps in to pay the rest (the remaining 20%).

The Pros of Medigap:

Ultimate Freedom of Choice: You can see any doctor, specialist, or hospital in the United States that accepts Original Medicare. There are no restrictive local networks. If you want to go to UPMC Altoona, Penn State Health, or even the Mayo Clinic, you can.

No Referrals Required: You do not need a referral from a primary care doctor to see a specialist.

Predictable Costs: Because your Supplement covers the gaps, your out-of-pocket medical costs are highly predictable. You won't be hit with a massive hospital copay if you get sick.

The Cons of Medigap:

Higher Monthly Premiums: You will pay a monthly premium for the Supplement which will often exceed $100/month.

Separate Part D Plan: You will also need to add on a standalone Part D prescription drug plan which comes with an additional premium.

No "Extra" Perks: Standard Medigap plans do not include routine dental, vision, or hearing coverage (although some may include a gym membership).

The Case for Medicare Advantage (Part C)

Medicare Advantage plans are offered by private insurance companies that bundle your Part A, Part B, and usually Part D (prescription drugs) into one plan.

While we lean toward the comprehensive protection of Medigap, Medicare Advantage plans certainly have a place - especially for cost-conscious consumers or those who rarely go to the doctor. For a deeper dive into how these plans work, check out our blog Exploring Medicare Advantage: A Beginner’s Guide.

The Pros of Medicare Advantage:

Low Monthly Premiums: Many plans in Central PA offer $0 monthly premiums.

Bundled Convenience: Your medical and prescription drug coverage are rolled into one insurance plan.

Extra Benefits: These plans often include perks that Original Medicare doesn't, such as dental allowances, vision exams, hearing aids, and gym memberships.

The Cons of Medicare Advantage:

Network Restrictions: You generally must use doctors and hospitals within the plan's local network. If your preferred specialist leaves the network, you may have to find a new doctor.

Prior Authorizations: The insurance company may require approval before you can get certain procedures, surgeries, or medications.

Higher Out-of-Pocket Exposure: If you get seriously ill, the daily copays for hospital stays, cancer treatments, and ambulance rides can add up quickly until you hit the plan's Maximum Out-of-Pocket (MOOP) limit.

✅ Agent Tip: Because of this out-of-pocket exposure, if you choose a Medicare Advantage plan, we highly recommend coupling it with a Hospital Indemnity Plan. This is an inexpensive policy that pays you cash if you are hospitalized, which you can use to cover those expensive Advantage plan copays.

Which is Better for You?

There is no one-size-fits-all answer, but here is a general rule of thumb:

A Medicare Supplement might be better if:

You want the peace of mind knowing your medical bills are covered if you get seriously ill.

You travel frequently or split your time between Pennsylvania and another state.

You want the freedom to see any doctor without worrying about networks or referrals.

You can comfortably afford a higher monthly premium in exchange for lower risk.

A Medicare Advantage plan might be better if:

You are generally healthy, rarely see the doctor, and want to save money on monthly premiums.

You are comfortable staying within a local network of doctors and hospitals.

You place a high value on extra benefits like dental, vision, and fitness memberships.

Need Help Deciding Between Medigap and Medicare Advantage?

Schedule your NO COST consultation today to get unbiased advice from a local Medicare expert!

Summary

Although we tend to favor Medigap as it typically delivers stronger overall protection and less financial exposure, Medicare Advantage plans are a practical choice for cost-sensitive consumers or people who rarely seek medical care.

Our best advice: get local, unbiased assistance! Choosing between Advantage and Medigap is a big decision, and you don't have to make it alone. National 1-800 call centers don't know the local doctor networks in Altoona, Hollidaysburg, or Duncansville - but we do. At Care Compass, our goal is education, not a sales pitch. We represent the top carriers in Pennsylvania, but we remain independent advisors, working to help you understand your options and choose the best plan for your needs. And the best part? There is NO COST to use our services.

Schedule a NO COST Consultation with Tara today! Let's sit down, look at your specific doctors and medications, and find the path that gives you the best coverage and peace of mind.

Care Compass is an independent insurance agency that helps seniors navigate the complexities of Medicare and other Senior Products. Our services are offered at NO COST! Care Compass is proudly owned and operated in Blair County, Pennsylvania. We provide Medicare insurance assistance to the residents of Altoona, Hollidaysburg, Duncansville and the surrounding region. If you need assistance with Medicare, contact Care Compass today!